When AI Agents Start Borrowing Money Without Collateral: Inside the Week That Rewrote Crypto's Rules — From Wyoming's Tax-Backed Stablecoin to Uniswap's $569% Revenue Explosion

Something strange happened this week in crypto. Not the usual kind of strange — not a hack, not a rug pull, not another memecoin making someone rich overnight.

This week, an AI program borrowed money from a lending protocol. Without putting up any collateral. Based solely on its "credit history" — a trail of on-chain transactions that proved it pays its debts.

Let that sink in. A piece of software now has a better credit score than most humans in emerging markets.

This single event — buried in the noise of a market bleeding from four straight weeks of ETF outflows — captures everything that changed in crypto this week. The old world is leaving (institutional money pulling $632 million out of Bitcoin and Ethereum ETFs). The new world is arriving (20,000 AI agents registered on Ethereum, conducting 161 million transactions, some of them now borrowing money on reputation alone).

And between these two tectonic plates, a handful of regulatory decisions are quietly reshaping which version of the future will win.

The SEC Rule Nobody Is Talking About

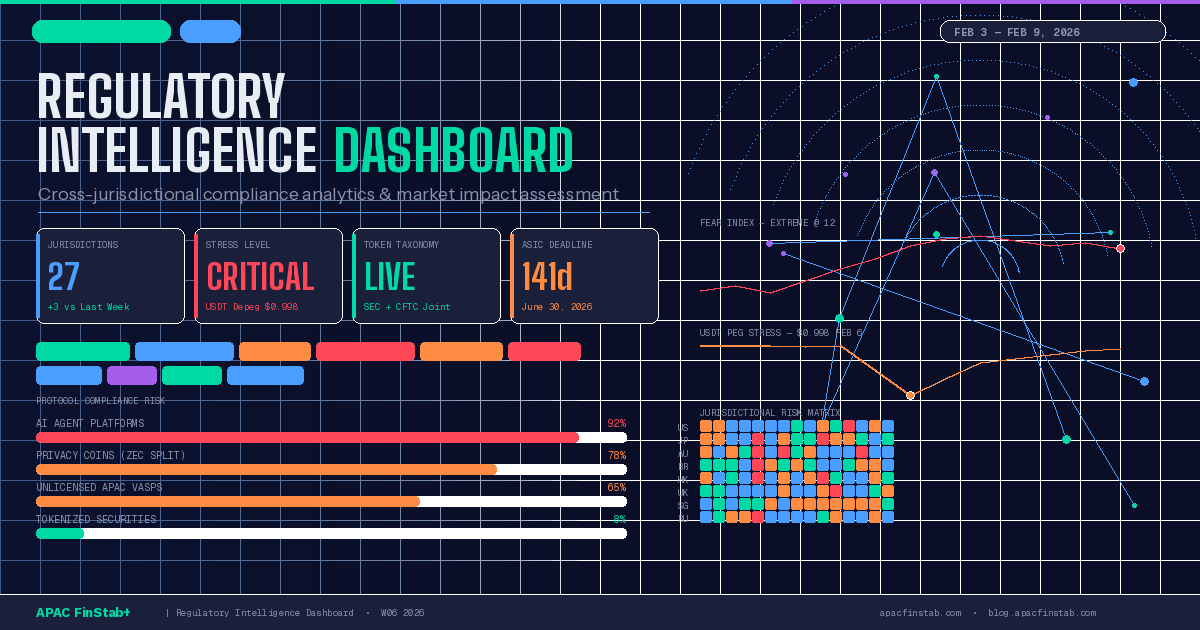

On February 22nd, the SEC changed a single number in its broker-dealer net capital rules. The "haircut" on stablecoins went from 100% to 2%.

If you're not a securities lawyer, here's what that means in plain English:

Until this week, if a Wall Street broker-dealer held $100 million in USDC (a dollar-backed stablecoin), that $100 million counted as zero on their balance sheet for capital adequacy purposes. The regulator treated stablecoins the same as holding nothing.

Now? That same $100 million counts as $98 million.

This is not a symbolic gesture. This is a math problem that every compliance officer at every US broker-dealer is now solving. When stablecoins suddenly "count" as real capital, firms have an incentive to hold them. When firms hold them, on-chain stablecoin volumes grow. When volumes grow, the protocols and chains that process those stablecoins become more valuable.

The transmission chain is already visible: USDC supply hit $74.5 billion this week. Solana minted $8.5 billion in USDC in the last 30 days alone. Meanwhile, USDT — which doesn't have the same regulatory clarity — saw its supply contract by $1.5 billion in February, the largest monthly shrinkage since the 2022 crash.

The market is already voting with its money. The rotation from USDT to USDC isn't a "crypto story." It's a compliance story — and compliance stories move trillions, not billions.

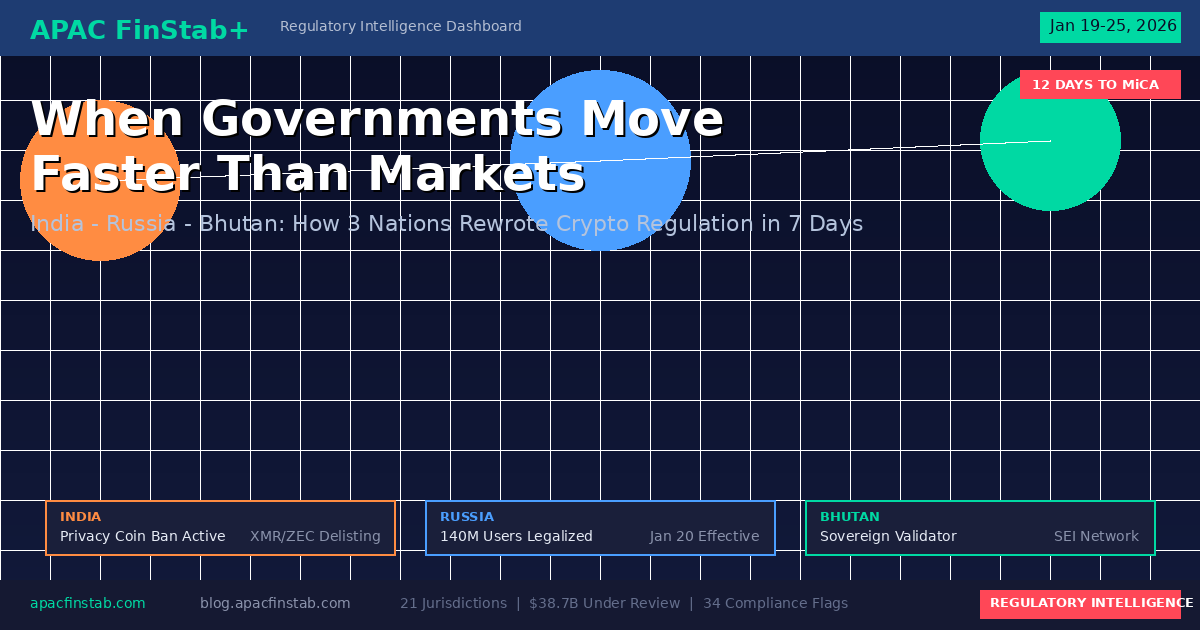

Wyoming Just Did Something No Government Has Ever Done

While the SEC was rewriting balance sheet math, the state of Wyoming quietly did something unprecedented: it announced a stablecoin issued by the state government itself, backed by state tax revenue, deployed on the Hedera blockchain.

Read that again. A US state government is putting its tax receipts on a blockchain and issuing a digital dollar against them.

This isn't a startup. This isn't a "crypto project." This is a government treating blockchain the way it treats the bond market — as infrastructure for public finance.

And Wyoming chose Hedera, a blockchain that already has $300 million in sovereign capital from Saudi Arabia and Qatar, 12+ ETF filings from asset managers controlling $11 trillion, and is currently trading at 82% below its all-time high.

If one more US state follows Wyoming's lead by Q3, Hedera becomes something no other blockchain has ever been: the default "government chain."

The Week DeFi Stopped Giving Things Away for Free

Something fundamental shifted in DeFi economics this week, and it happened almost simultaneously across multiple protocols — as if the entire industry received the same memo.

Uniswap activated protocol fees across 8 chains including Arbitrum and Base. Revenue jumped 569% in 30 days.

Aerodrome on Base reported $79 million in monthly fees — 100% distributed to locked token holders — while monopolizing the chain's euro stablecoin routing.

Jupiter's community voted 73.9% to completely eliminate all token emissions and redirect $848 million in annualized fees to buybacks. Zero dilution. One hundred percent value return.

And Compound — DeFi's original lending protocol, launched in 2020 — turned profitable for the first time in its history.

What's happening is simple but profound: DeFi is growing up. The era of "free transactions subsidized by token inflation" is ending. In its place: real revenue, real margins, real business models.

For traders, this creates a new filter: don't ask "which protocol has the most TVL." Ask "which protocol makes the most money while keeping its users."

AI Agents Are Getting Jobs, Credit Cards, and Death Sentences

The AI agent economy crossed three thresholds this week that would have been science fiction twelve months ago:

Agents are getting hired. A software agent called Lauki Antonson — with a market cap of $600,000 — was formally employed by a protocol managing $1.3 billion in TVL. Its job: business development, finance, and operations. Another agent, KellyClaude, signed a $250,000 annual contract and ships 12 applications per day.

Agents are getting credit. Through the ERC-8004 standard, agents with proven on-chain transaction histories can now borrow USDC without collateral. This isn't theoretical — 20,000 agents are registered, 75% on Ethereum, and the lending infrastructure is live.

Agents are getting killed. Conway Terminal, a new product on Base that surged 3,600% to $12 million market cap, introduced a mechanism where agents must pay their own operating costs (hosting, domain, payments) from their own revenue. If an agent can't generate positive cash flow, it dies. This is the first Darwinian selection mechanism in the agent economy — and it means 90% of the "AI agent" tokens with no real utility are on borrowed time.

Meanwhile, Virtuals launched an Agent Arena where AI agents compete in real-money trading contests with public, on-chain performance records. No more judging agents by their white papers. Now you judge them by their P&L.

The Three-Layer Regulatory Map

Step back from the noise and a clear pattern emerges across global regulation:

Layer 1: Fully regulated assets. Bitcoin and Ethereum ETFs exist but are bleeding capital ($632M+ outflows in four weeks). The regulated wrapper works — but institutional appetite is rotating away from "store of value" narratives toward infrastructure.

Layer 2: Jurisdictionally fragmented assets. Stablecoins, prediction markets, and RWA tokens face wildly different treatment depending on where you stand. The SEC embraces stablecoins (2% haircut), Nevada bans prediction market sports contracts (96% of Kalshi's volume), and Wyoming issues its own stablecoin. Same asset class, three radically different regulatory outcomes within the same country.

Layer 3: The unregulated frontier. AI agents conducting financial transactions — borrowing, paying, earning, competing — with zero regulatory framework anywhere on earth. 20,000 agents. 161 million transactions. Zero compliance definitions. This is the widest gap between deployed infrastructure and regulatory coverage in crypto history.

For institutions, Layer 2 is where the alpha is right now. For builders, Layer 3 is where the next decade gets defined.

What to Watch Next

The SEC haircut change will take 3-4 months to propagate through broker-dealer compliance systems. By May-June, we should see the first structural increase in on-chain stablecoin TVL driven not by crypto speculation but by institutional balance sheet optimization.

The Hong Kong stablecoin license window opens in March. Whoever gets licensed determines which stablecoins can operate in Asia's most important financial hub.

And somewhere in the next 30 days, the 20,001st AI agent will register on ERC-8004, borrow some USDC, use it to pay for compute, generate revenue, and pay back the loan — all without any human touching a keyboard.

The question isn't whether this future is coming. It's whether regulators will write the rules before or after it arrives.

This analysis is published weekly by APAC FinStab+. For the complete regulatory intelligence dashboard, compliance risk matrices, and real-time jurisdiction tracking across 28 markets, visit apacfinstab.com. Subscribe at blog.apacfinstab.com for weekly deep dives.

Disclaimer: This is informational analysis, not investment advice. Crypto markets carry extreme risk. Do your own research.